How Easy is It to Get a Heloc

What is a home equity line of credit?

A home equity line of credit, or HELOC, is a second mortgage that gives you admission to cash based on the value of your dwelling. Y'all can draw from a home equity line of credit and repay all or some of information technology monthly, somewhat similar a credit card.

With a HELOC, yous borrow against your disinterestedness, which is the domicile's value minus the amount you owe on the master mortgage. Yous can too get a HELOC if you own your dwelling house outright, in which example the HELOC is the primary mortgage rather than a second i.

How a HELOC works

Much like a credit carte that allows you to infringe confronting your spending limit as often as needed, a HELOC gives you the flexibility to borrow against your home equity, repay and repeat.

Well-nigh HELOCs accept adaptable involvement rates. This means that as baseline interest rates go up or down, the interest rate on your HELOC will adjust, too.

To set your charge per unit, the lender will get-go with an index rate, then add a markup depending on your credit profile. Generally, the higher your credit score, the lower the markup. That markup is chosen the margin, and y'all should ask to see the amount before you sign off on the HELOC.

HELOC requirements

Lender requirements will vary, but hither's what you'll generally need to get a HELOC:

-

A home value that'southward at least 15% more than you owe.

How to get a habitation equity line of credit

The process of getting a HELOC is like to that of a buy or refinance mortgage. You'll provide some of the aforementioned documentation and demonstrate that you're creditworthy. Here are the steps you'll follow:

-

One time you accept pulled together your documentation and selected a lender, apply for the HELOC.

-

You'll receive disclosure documents . Read them advisedly and ask the lender questions. Brand sure the HELOC volition fit your needs. For example, does it require you to borrow thousands of dollars upfront (often called an initial draw)? Do you have to open a split up bank account to go the best rate on the HELOC?

-

The underwriting process, though not as extensive as when you got your mortgage, can take weeks.

-

The final stride is the loan closing, when you sign paperwork and the line of credit becomes bachelor.

Nerdy tip: Don't assume that the price y'all paid at closing is what your home is worth. During underwriting, your lender may order an appraisal to ostend the habitation's value. If home prices in your area have appreciated while you've endemic your home, yous'll besides have more equity, as the divergence between the holding'south higher value and the amount remaining on your mortgage will be larger.

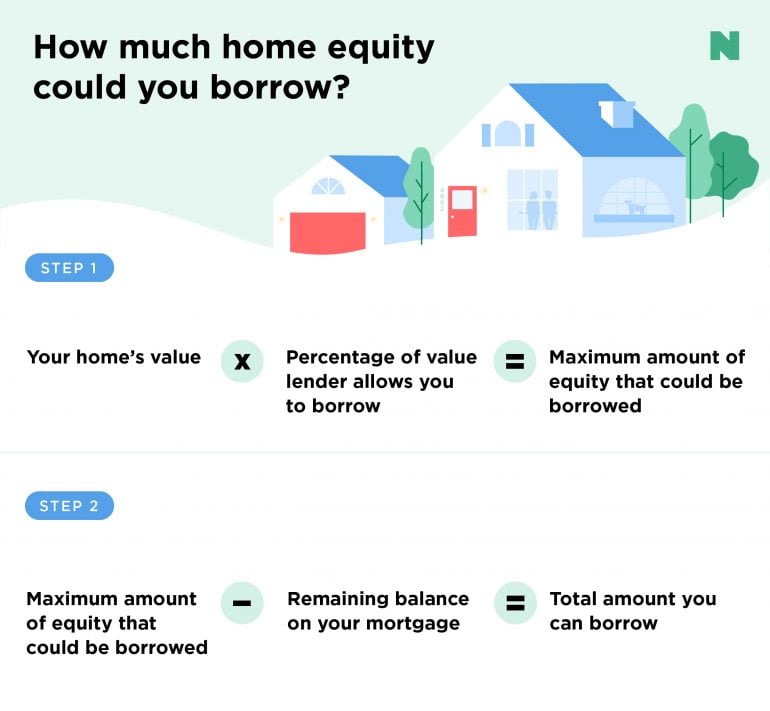

How much can you borrow?

The maximum amount of your home equity line of credit volition vary based on the value of your home, what percentage of that value the lender will allow you lot to borrow confronting and how much you nevertheless owe on your mortgage. Two quick calculations can give you lot an idea of what you might be able to borrow with a HELOC.

Your home'southward current value x Pct of value lender allows yous to borrow = Maximum amount of equity that could exist borrowed

Maximum amount of equity that could be borrowed - Remaining balance on your mortgage = Total amount you tin borrow

Say you take a home currently worth $300,000 with a rest of $200,000 on your showtime mortgage, and your lender will allow you to admission up to 85% of your home's value. Multiplying the home's value ($300,000) past the pct the lender will allow you to borrow (85%, or .85) gives you a maximum corporeality of $255,000 in equity that could be borrowed. Subtract the amount y'all still owe on your mortgage ($200,000) to get the total amount y'all can borrow with a HELOC — $55,000.

Or skip doing the math, and use the HELOC calculator beneath to come across how much you might be able to infringe.

How you lot pay back a HELOC

A HELOC has 2 phases: the draw period and the repayment period.

Describe period: During the draw flow, you lot can infringe from the credit line by check, transfer or a credit card linked to the account. Monthly minimum payments often are interest-simply during the draw catamenia, but you tin can pay principal if you wish. The length of the draw menstruation varies; information technology's oftentimes ten years.

Repayment flow: During the repayment menses, yous can no longer infringe confronting the credit line. Instead, y'all pay back the loan in monthly installments that include main and interest. With the addition of principal, the monthly payments can rise sharply compared with the draw flow. The length of the repayment period varies; it'southward often 20 years.

At the end of the loan, yous could owe a large lump sum — or balloon payment — that covers whatsoever principal non paid during the life of the loan. Before you close on a HELOC, consider negotiating a term extension or refinance pick so that you're covered if you tin can't beget the lump sum payment.

Nerdy tip: If yous plan to move whatsoever time soon, a HELOC may non exist the right selection for you. When yous sell your home, yous'll have to pay off the balance of the HELOC (after all, you tin't infringe the disinterestedness of a home y'all don't own). Paying off the home equity line of credit could cutting into whatever profits you lot might be making from your habitation'due south auction. You might likewise have to pay a cancellation fee to the lender.

Is getting a HELOC a adept idea?

Whether a home disinterestedness line of credit is a proficient idea really comes down to your goals and fiscal state of affairs. A HELOC is often used for dwelling repairs and renovations, which can increase your home's value. Some other bonus: The involvement on your HELOC may be tax-deductible if yous use the money to purchase, build or substantially improve your home, according to the IRS.

Some use domicile equity lines of credit to pay for education, but you may get better rates using federal student loans . Financial advisors generally don't recommend using a HELOC to pay for vacations and cars because those expenditures don't build wealth, and may put you at risk of losing the abode if you default on the loan.

Disadvantages of a home equity line of credit

The main drawback of a HELOC is that it increases the take chances of foreclosure if you tin can't pay the loan. Regardless of your goal, avoid a HELOC if:

Your income is unstable. If it's possible that your income will change for the worse, a HELOC may be a bad thought. If you tin't keep up with your monthly payments, your lender could force you out of your home.

You tin't beget the upfront costs. A HELOC may require an application fee, title search, home appraisal, existent manor chaser fees and points. These charges tin can prepare y'all back hundreds of dollars.

You aren't looking to infringe much coin. A HELOC's upfront costs may non be worth it if you need only a small-scale line of credit. In that case, yous may be better off with a low-involvement credit carte , possibly with an introductory involvement-free flow.

You can't beget an interest charge per unit increase. HELOCs have adjustable rates. The loan paperwork will disembalm the lifetime cap, which is the highest possible rate. Could you afford a monthly payment with that much interest? If not, call up twice near getting the loan.

You're using it for basic needs. If you need extra money for 24-hour interval-to-day purchases and you're having problem simply making ends run across, a HELOC isn't worth the hazard. Information technology's safer to become your finances in shape before taking on additional debts.

Variable rates leave you vulnerable to rise interest rates. Exist sure to take this into account. Wait at the size of the periodic cap (that's how much the interest rate tin modify at any 1 time) and the lifetime cap (the highest interest charge per unit yous could be charged over the life of the loan) to get an idea of how loftier your payments could get.

On the plus side, as with a credit card, you pay interest only on the amount of money yous use, not the total credit line available to borrow.

Getting the all-time HELOC rate

This 1's on you: The more you lot enquiry, the bigger your reward. As you look for the all-time HELOC rates, get quotes from various lenders. Check your primary bank or mortgage provider; it might offering discounts to existing customers. Get a quote and compare its rates with at to the lowest degree two other lenders. As y'all shop around, take note of introductory offers similar initial rates that volition elapse at the terminate of a given term.

How a HELOC affects your credit score

Although a HELOC acts a lot similar a credit card, giving you ongoing admission to your home'south disinterestedness, at that place's one big difference when it comes to your credit score : Some bureaus treat HELOCs of a certain size like installment loans rather than revolving lines of credit.

This means borrowing 100% of your HELOC limit may non have the same negative effect as maxing out your credit card. Like any line of credit, a new HELOC on your report will likely reduce your credit score temporarily. However, if y'all borrow responsibly — making timely payments and not utilizing the full credit line — your HELOC could help y'all improve your credit score over fourth dimension.

Is information technology meliorate to get a home equity loan or line of credit?

That depends on your financial situation and needs. A HELOC behaves similar a revolving line of credit, letting you tap your home's value in the amount you demand as you need information technology. A home equity loan works more like a conventional loan, with a lump-sum withdrawal that'south paid back in installments.

HELOCs typically accept variable interest rates, while dwelling house equity loans are normally issued with a stock-still interest rate. This can salve you from a futurity payment shock if interest rates ascent. Work with your lender to decide which choice is best for your financing needs.

Oftentimes asked questions

A habitation equity line of credit, or HELOC, is a type of second mortgage that lets you borrow confronting your home equity. Somewhat like with a credit card, y'all employ coin from the HELOC as needed, then pay information technology back over fourth dimension.

With a HELOC, instead of borrowing a lump sum, yous borrow money when you need it. Though your full credit line may be substantial, yous only pay interest on the funds y'all actually utilise. HELOCs more often than not have adjustable interest rates, and so HELOC rates fluctuate forth with the market.

How is a HELOC paid back?

A HELOC has two phases, known as the draw period and the repayment period. During the draw catamenia, you borrow money as needed, and required monthly payments generally just cover interest. In the repayment period, you can no longer borrow coin, and you'll pay back both the principal and the interest.

Is HELOC interest taxation deductible?

You may be able to claim a tax deduction on your HELOC interest if you used the loan for home improvements. The IRS sets annual limits that vary depending on whether you're unmarried, head of household or filing jointly, and yous'll have to itemize your deductions in society to have advantage of this one.

What is a HELOC?

A home equity line of credit, or HELOC, is a blazon of

second mortgage

that lets yous borrow against your home equity. Somewhat similar with a credit card, you apply money from the HELOC as needed, then pay it dorsum over time.

How does a HELOC work?

With a HELOC, instead of borrowing a lump sum, y'all borrow money when you need it. Though your total credit line may be substantial, you only pay interest on the funds you actually use. HELOCs generally have adjustable interest rates, so

HELOC rates

fluctuate along with the marketplace.

How is a HELOC paid back?

A

HELOC

has two phases, known every bit the describe flow and the repayment period. During the draw menses, you borrow coin as needed, and required monthly payments generally just cover interest. In the repayment period, you tin can no longer borrow coin, and y'all'll pay dorsum both the principal and the involvement.

Is HELOC interest tax deductible?

You lot may be able to claim a

tax deduction

on your HELOC interest if you used the loan for home improvements. The IRS sets annual limits that vary depending on whether you lot're single, head of household or filing jointly, and yous'll have to catalog your deductions in social club to take advantage of this one.

Source: https://www.nerdwallet.com/article/mortgages/heloc-home-equity-line-of-credit